completed

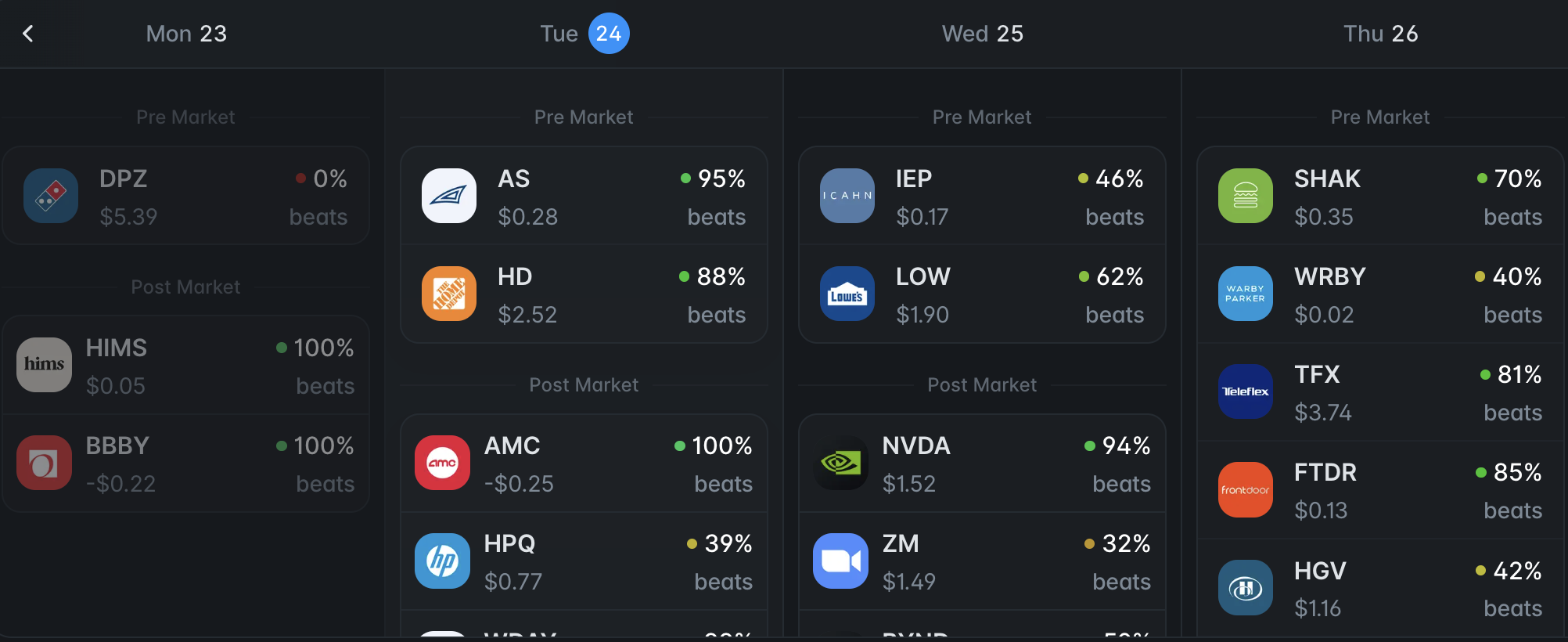

Polymarket Earnings Prediction

pythonmachine-learningxgboostpolymarket

I'm Ibrahim Fırat Soysal, a Master of Finance student at Fordham University with a relentless obsession for quantitative modeling and predictive systems.

I build at the intersection of finance and machine learning, focusing on identifying mispriced events in prediction markets through NLP and statistical inference. This notebook is where I document my research, open-source projects, and algorithmic approaches to high-variance probability markets.

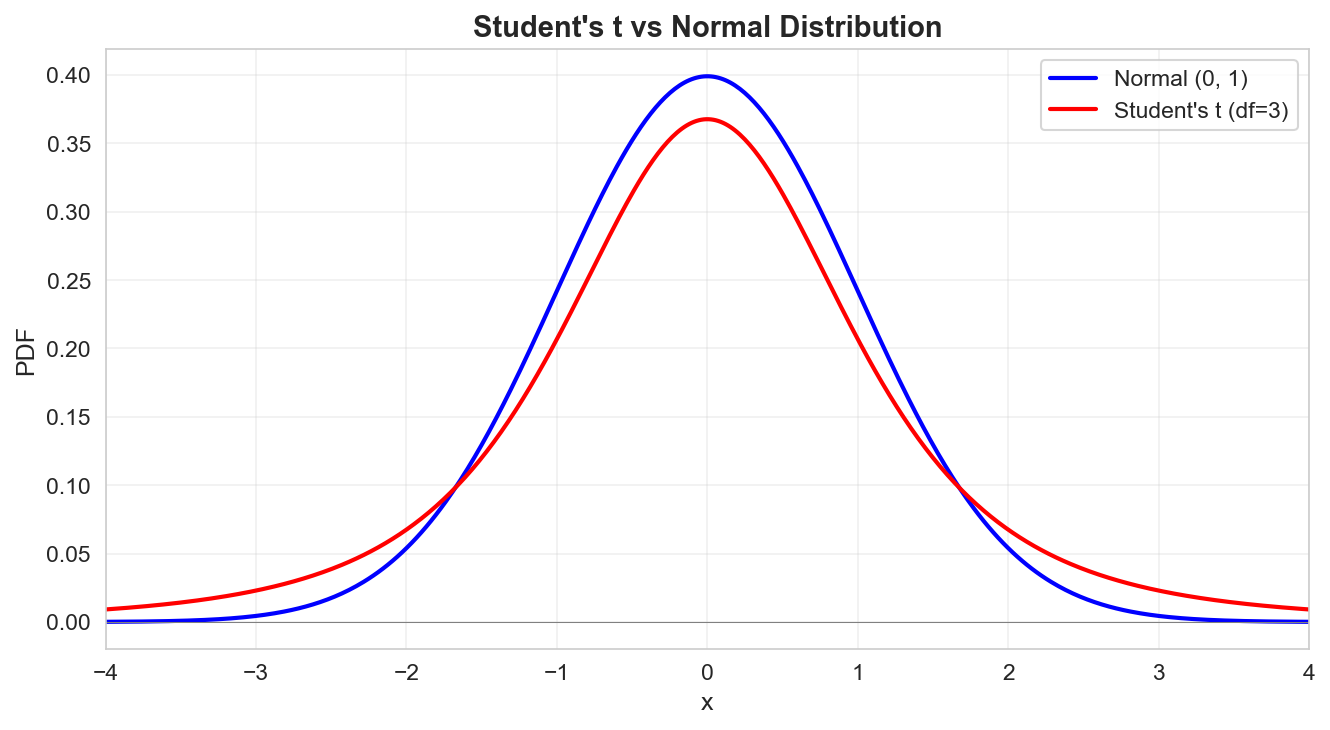

Adjust the standard deviation to see how tail risk scales.